Listen to this Fuel for Thought

podcast

As EV sales slow, OEMs must consider multiple factors to

align their EV production with government regulations and consumer

demand.

Insights in this Newsletter & Podcast:

-

The pathway to electrification: from the here-and-now reality to

the long-term aspiration of decarbonization in the transportation

sector. -

The US government regulatory aspirations and their pressure on

OEMs towards an accelerated response to electrification. -

The consumer mindset and sentiment towards electrification:

pricing, technology and the willingness of adoption. -

OEM showroom response to align regulation and pricing via

alternative vehicle electrification pathways.

The first quarter of 2024 brought significant attention to the

tapering of electric vehicle (EV) momentum in the United States,

with many clamoring “I told you so.” There is no question that

aligning the current administration's aspirations of a decarbonized

transportation sector to the reality of how consumers transition

towards electrified vehicles will remain very fluid. Much of this

chapter of history will be written in the coming decade and is

likely to feature surprises as the industry is shifting very

quickly to a known emerging technology with an unknown consumer

response. As a result, it is important to separate today's

front-page news of early adopters from the mid-term ramp up and

eventual long-term stabilization of EVs in the marketplace. It's

also critical that all stakeholders are aware that failure to

electrify is not an option.

Light vehicle sales in the US closed the first quarter at an

estimated 15.4 million-unit SAAR, featuring growth of 5.4%

year-over-year. The market is also transitioning from a

build-to-order model back to a business-as-usual world of

inventories and incentives for most segments. From a propulsion

perspective, the market share for EVs is largely unchanged

year-over-year. This is starkly different from the 50% expansion of

2023 and the first time in many years where EV growth has tapered

to the single-digit level.

The stagnation of EV sales is making many within the industry

uncomfortable (OEMs and suppliers alike) as the ongoing ramp-up of

EV production capacity requires a continuous robust expansion of

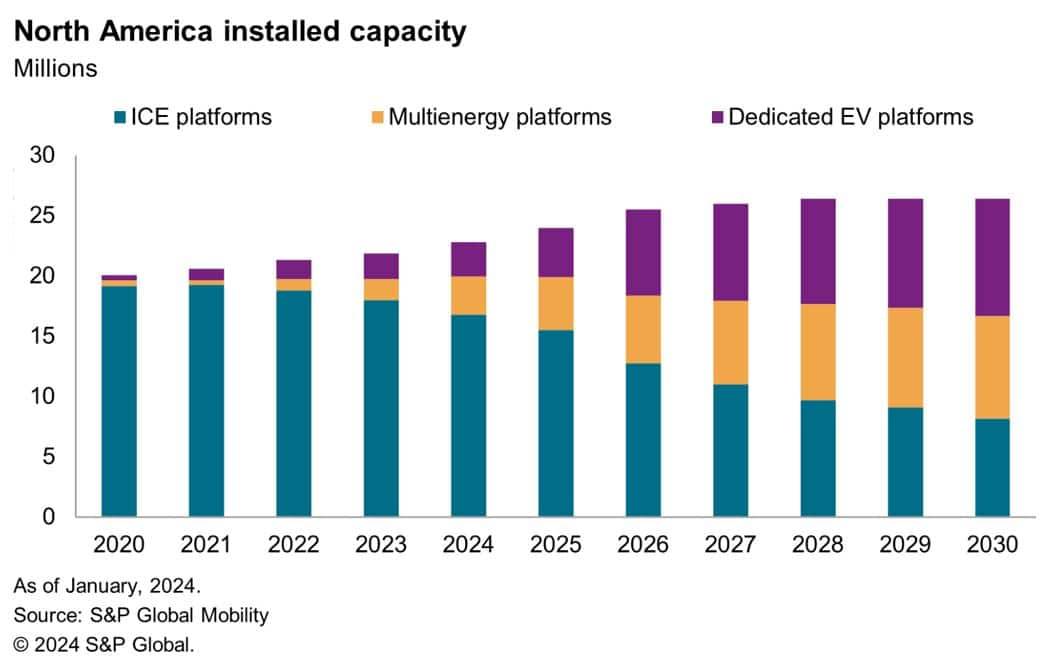

electrification. Capacity in North America is roaring from 20

million units today to 26 million within the next few years, as all

OEMs want to proactively respond to regulatory requirements.

Roughly 20 plants are expected to start or restart operations this

decade (since 2020) geared towards ZEV assembly and dozens more are

retooling their production from ICE to ZEV platforms.

This capacity expansion is pointing toward an industry

migration—with more than 65% of North America-manufactured

vehicles expected to be electric by 2030. However, the mood is

cautionary for many OEMs with a manufacturing base in North America

as they try to match government ambitions of a 50% Zero-Emission

Vehicle (ZEV) market by 2030 (roughly a six-fold expansion in a

six-year period) alongside weaker consumer demand. This alignment

is only aggravated as it comes on the tails of a newly minted labor

agreement that will boost wages by over 25% through 2027 for most

plants in the US and Canada and is likely to erode

profitability.

It is also important to mention that the Biden administration

understood that matching a 50% ZEV regulatory target would need

support. Simply put, this was going to be a carrot-and-stick

approach, with the carrot being the Inflation Reduction Act (IRA).

The IRA has multiple components supporting the path to

decarbonization in the U.S.; the most critical to the automotive

industry are the consumer and manufacturer credits for purchase and

production of ZEV vehicles. Putting these two together could

represent an average stimulus of $12,090 for ZEVs that meet all

requirements, assuming a full $7,500 consumer credit and a $4,590

manufacturer credit ($45 per kW on the average US battery size of

102 kW for 2022).

This approach triggered unparalleled investment for the

expansion of ZEV capacity. OEMs assumed if they built them (EVs)

they (consumers) would come. It was only natural to assume that the

strong consumer demand for EVs seen in California and many other

West Coast markets was going to expand across the country if IRA

funds helped to close the gap in price between ZEVs and legacy

Internal Combustion Engine (ICE) vehicles. OEMs have worked very

hard to match the success Tesla is having in these markets,

especially after the EV juggernaut's Model Y was the third

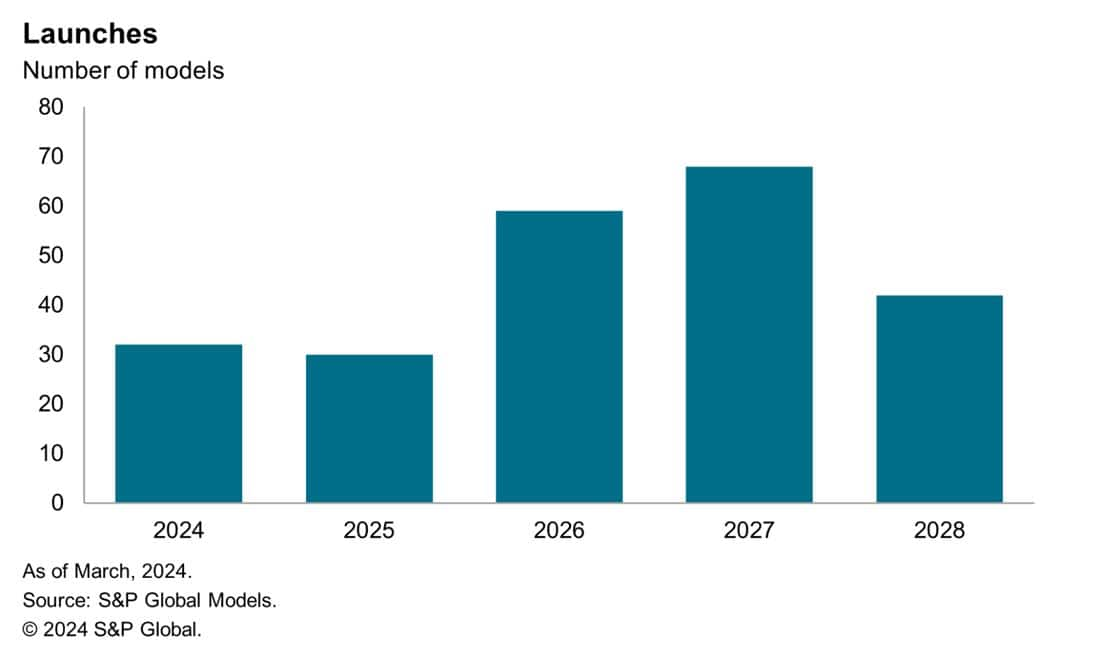

top-selling light vehicle last year. The response from OEMs is a

pipeline of over 30 different new EV models due in 2024 and more

than 200 models due by 2028, according to current forecasts.

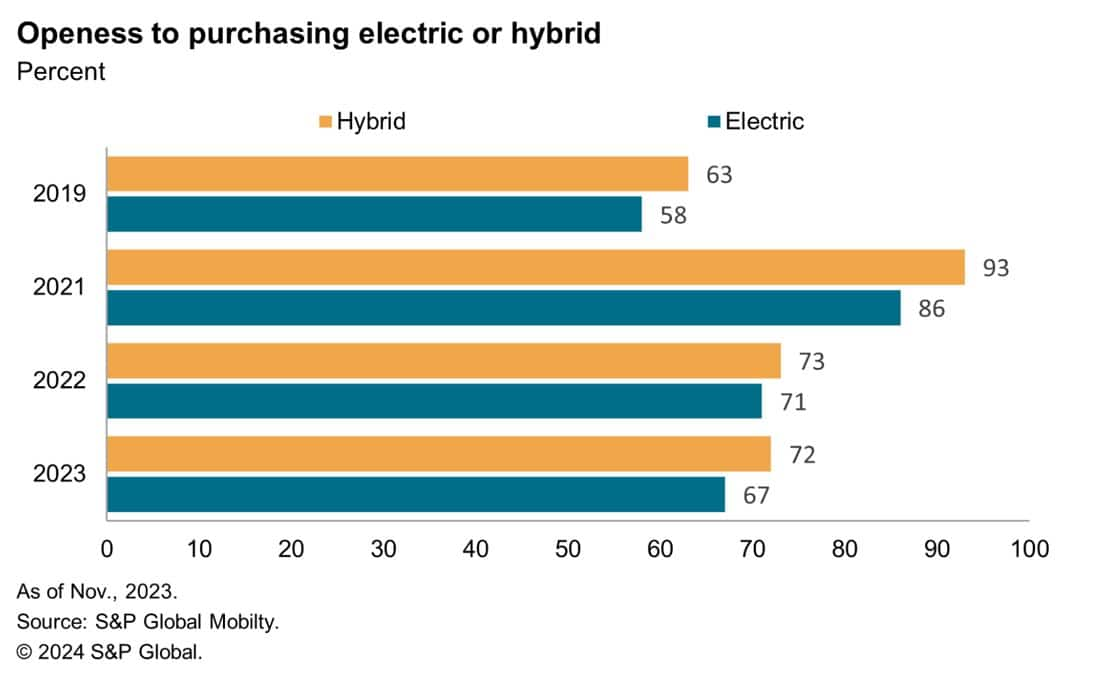

To understand consumer behavior and mindset, S&P Global

Mobility runs proprietary surveys on a regular basis, one of which

measures EV consumer sentiment. This research essentially

recognizes the willingness of consumers to buy EVs. Our 2023 survey

showed a 67-percent willingness to consider buying an EV vehicle,

though a 19-percentage-point decline relative to the same survey in

2021 when EV excitement was cresting in the middle of the

inventory/semiconductor crisis. Our 2023 survey indicates the

primary concerns consumers had in mind were pricing, range and

charging.

This same survey shows that consumers prefer a gentler

transition towards electrification—more of an evolution than

revolution. Here, hybrids are clearly top of mind to consumers

where the need to change is not as drastic—essentially

remaining on the same fueling system they are familiar with. It has

only been in recent months that we have seen some OEMs assimilate

this reality and reconsider their pathway to electrification.

The electrification roadmap will be primarily dependent on the

triangulation of these three elements: pricing of EVs, meeting

regulatory requirements from the government, and OEMs' creativity

and flexibility to adjust their showroom portfolios to best match

these two. Some OEMs are realigning strategies to create a bridge

in the shape of Hybrid Electric Vehicles (HEV) and Plug-in Hybrid

Electric Vehicles (PHEV) to address consumer concerns of pricing,

range, and charging for EVs. This comes after traditional OEMs are

now publicly stating that price parity for EVs won't be as easy as

originally envisioned and have gone back to the drawing board to

look for alternate roadmaps to appease consumer hesitation while

remaining good corporate citizens.

Historically the law of the land has revolved around

miles-per-gallon and meeting the regulatory requirement has been no

small feat over the last two decades as it required an average 5%

improvement in efficiency year-over-year. In response to lowering

carbon emissions in the US, the Biden administration has added new

dimensions to that equation by proposing a revised setting of e-MPG

(equivalent MPG rating for EVs and PHEVs) and the requirement to

also reduce emissions of other pollutants. From a numeric

standpoint, if an EV used to get a 350 e-MPG rating the revision to

the e-MPG calculation means that same vehicle will only be getting

roughly 125 e-MPG rating in coming years.

To most, this is already a very tall order to meet, but again,

times are very fluid. The roadmap of electrification becomes even

more challenging as it may have to accommodate for a long list of

what-ifs: US presidential elections, cost of raw materials, a

revision of USMCA, or other factors. This accommodation and

flexibility demand that OEMs respond quickly and, in the process,

shift their entire value chain at similar speed, starting with

suppliers, raw material providers, and logistics operators as

well.

The writing of this thrilling chapter of the automotive history

book as OEMs are asked to align pricing, regulation, and portfolios

will not be black and white, but a true prism of colors. Lack of

action is certainly not an option; the OEM ships have left the

ports in search of a new carbon-free world and are navigating

uncharted consumer waters and the perils that come along with such

an altruistic endeavor.

Rest assured, we at S&P Global Mobility look forward to

helping the industry best chart these waters to anticipate the

rough seas and storms ahead.

——————————————————————-

Dive deeper into these mobility insights:

Explore More Electric

Vehicle Trends

2024 US Presidential

Election and the Auto Industry – Read the article

Commercials Cooperation Advertisements:

(1) IT Teacher IT Freelance

立刻註冊及報名電腦補習課程吧!

电子计算机 -教育 -IT 電腦班” ( IT電腦補習 ) 提供一個方便的电子计算机 教育平台, 為大家配對信息技术, 電腦 老師, IT freelance 和 programming expert. 讓大家方便地就能找到合適的電腦補習, 電腦班, 家教, 私人老師.

We are a education and information platform which you can find a IT private tutorial teacher or freelance.

Also we provide different information about information technology, Computer, programming, mobile, Android, apple, game, movie, anime, animation…

(2) ITSec

www.ITSeceu.uk

Secure Your Computers from Cyber Threats and mitigate risks with professional services to defend Hackers.

ITSec provide IT Security and Compliance Services, including IT Compliance Services, Risk Assessment, IT Audit, Security Assessment and Audit, ISO 27001 Consulting and Certification, GDPR Compliance Services, Privacy Impact Assessment (PIA), Penetration test, Ethical Hacking, Vulnerabilities scan, IT Consulting, Data Privacy Consulting, Data Protection Services, Information Security Consulting, Cyber Security Consulting, Network Security Audit, Security Awareness Training.

Contact us right away.

Email (Prefer using email to contact us):

SalesExecutive@ITSec.vip