Listen

to the Fuel for Thought podcast.

With a slowdown in enthusiasm for battery electric vehicles,

the battery industry is wrestling with a combination of oversupply,

underutilization of capacity and lower return on investments.

Since the second half of last year, the electric vehicle segment

is facing strong headwinds, much to the surprise of many, as EVs

have been witnessing a strong demand in the last few years in

several markets around the world. The ambitious zero-emission (ZEV)

sales targets by both governments and automakers painted a rosy

picture about the EV industry and how quickly it is expected to

evolve.

As the novelty of EVs fades, the last several months have

brought forth the realization that there are still fundamental

issues that persist and need to be addressed for EVs to be a widely

accepted solution. Some of these issues are the lack of charging

infrastructure, long charging times and the high initial cost of EV

acquisition. Most of these challenges are not short-term and will

require years, if not decades to be fully solved.

What all the noise around EVs has led to is a massive investment

from many stakeholders in the EV ecosystem, right from material

sourcing to setting up significant manufacturing capacity for

batteries. The faster-than-realized uptake of EVs was expected to

propel the demand for batteries which necessitated a capacity

expansion to be able to able to meet the demand.

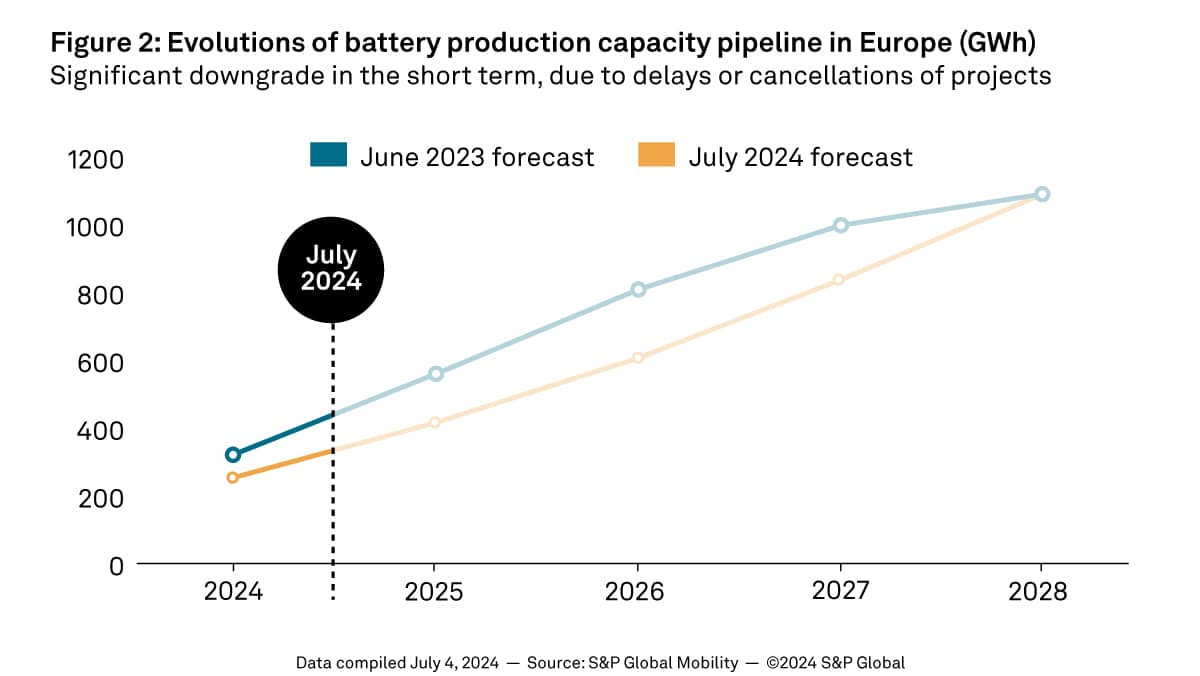

However, with the slowdown, the industry is now looking at a

case of oversupply, underutilization of the capacity and lower

return on investments.

Curtailing investments

From what has transpired in the industry in the last few months,

the OEMs and battery players have watered down their ambitions.

This has led to several reports and official announcements of

pulling back or postponement of investments in battery projects in

markets which were seen as the biggest growth centers for EVs.

Most recently, it was reported that Automotive Cells Company

(ACC), a joint venture by Stellantis, Total and Mercedes-Benz, has

decided to apply brakes on two of its upcoming EV battery plants in

Europe. The two plants are located in Kaiserslautern, Germany, and

in Termoli, Italy. Both plants were expected to have a production

capacity of 40 GWh each in 2030.

ACC also has a plant in Douvrin, France which is already in

production and is expected to start battery cell supply later this

year. Together, ACC had announced an investment of $7.6 billion in

the three plants. In the light of the slowdown, the three partners

are expected to review their investment plans by the end of the

year or early next year.

In fact, Mercedes-Benz has also announced a delay in its

electrification plans, pushing back its goal of 50% electrified

vehicle sales by five years. In 2021, Mercedes-Benz had said that

it will have 50% electrified vehicle sales (BEVs and hybrids) by

2025, which is now expected to be reached in 2030.

Earlier in May, mainland Chinese cell maker Svolt also announced

that it is dropping plans to set up a plant in Germany. In 2022,

Svolt had said that it will set up a 16 GWh cell plant in

Lauchhammer, Brandenburg to cater to European demand. The plant was

scheduled to start production in 2025. The tariff of mainland

Chinese players in Europe also played a role in Svolt taking this

decision.

Volkswagen too has said that it will hold back from taking a

decision on its fourth battery plant in Europe. The automaker was

aiming to set up a new battery plant in Eastern Europe and was

looking at Czech Republic, Hungary, Poland or Slovakia as possible

locations.

“Most of the European cell manufacturing projects are currently

facing challenges due to the recent slowdown in battery-electric

vehicle (BEV) sales. The investments made in new projects, or the

expansion of existing facilities were based on the expectation of

continued astronomical growth rates in recent years. However, the

poor performance of BEV sales in 2024 has resulted in a surplus of

unused capacities for cell makers. The significant price gap

between European batteries, which primarily rely on NCM technology,

and LFP cells from China further complicates the situation for

European cell makers, especially as car manufacturers strive to

introduce affordable electric vehicles,” said

Ali Adim, Manager, Technical Research, S&P Global

Mobility.

Europe is not the only region where an investment slowdown is

being witnessed. Several reports suggest that OEMs and battery

players are also delaying their investments in North America.

American automaker Ford also brought its battery investments

plans back to review board. Last November, Ford announced scaling

back of its Michigan plant in the US.

“While we remain bullish on our long-term strategy for electric

vehicles, we are re-timing and resizing some investments. As stated

previously, we have been evaluating BlueOval Battery Park Michigan

in Marshall. We are pleased to confirm we are moving ahead with the

Marshall project, consistent with the Ford+ plan for growth and

value creation. However, we are right sizing as we balance

investment, growth, and profitability. The facility will now create

more than 1,700 good-paying American jobs to produce a planned

capacity of approximately 20 GWh,” Ford said in a statement in

November 2023.

BlueOval Battery Park Michigan is a $3.5 billion investment by

Ford Motor Company which will produce lithium iron phosphate (LFP)

batteries that will power a variety of Ford's next-generation EV

passenger vehicles and pickups. Previously, the plant was set to

manufacture 35GWh of batteries and employ 2,500 people.

There also have been reports that Panasonic, one of the biggest

cell manufacturers in the United States, may also delay investing

in additional capacity of battery plants in North America.

Panasonic was reportedly planning to set up a third plant in the

US. However, the delay in investment may have put the plans for the

third plant in a limbo. “There's a need to control the speed of

investment depending on the speed at which EVs spread,” Yuki

Kusumi, Panasonic group's chief executive, was quoted as

saying.

There have also been reports that suggest Northvolt may delay

setting up its plant in Montreal, Canada, which was expected to

become operational by 2026.

Northvolt recently hit another roadblock when BMW, one of its

biggest customers, reportedly cancelled its €2 billion order for EV

lithium-ion battery cells. The supply of the cells, which were to

be produced in Europe at the Northvolt gigafactory at Skellefteå in

northern Sweden, was scheduled to start in 2024. Although

production delays were cited as one of the reasons for

cancellation, BMW may also be reviewing its cell demand, given the

slowdown in EV sales.

The cooling down of demand has also led to a significant drop in

the prices of critical battery raw materials such as nickel cobalt

and lithium. According to S&P Global, Prices for lithium,

nickel and cobalt sharply decreased in 2023 and are expected to

decline further in 2024.

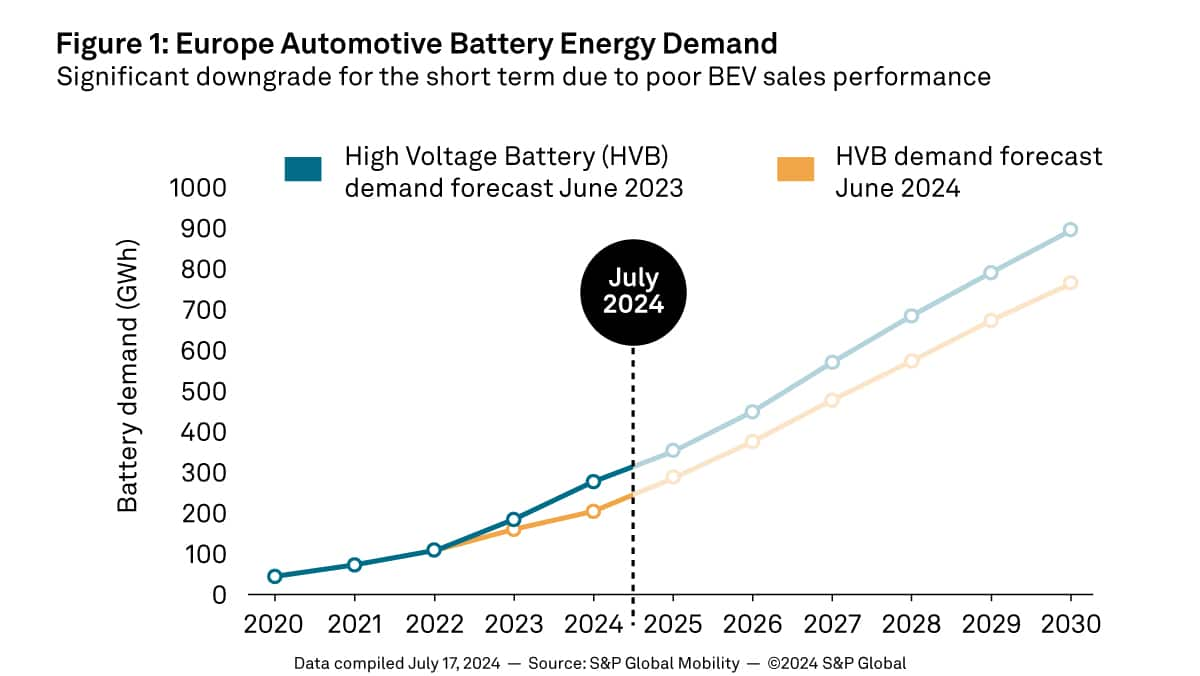

High voltage battery forecast

data.

By Srikant Jayanthan, Senior Research Analyst II, S&P Global

Mobility