Over the last 18 months, there has been a significant shift

toward leasing for electric vehicles in the United States —

driven both by market dynamics and federal legislation.

Looking first at industry dynamics, vehicle inventories have

grown as the pandemic and microchip shortage have receded. These

changes have also shifted the market from a seller's market to a

buyer's market. As buyers have gained more leverage, downward

pressure on pricing has intensified.

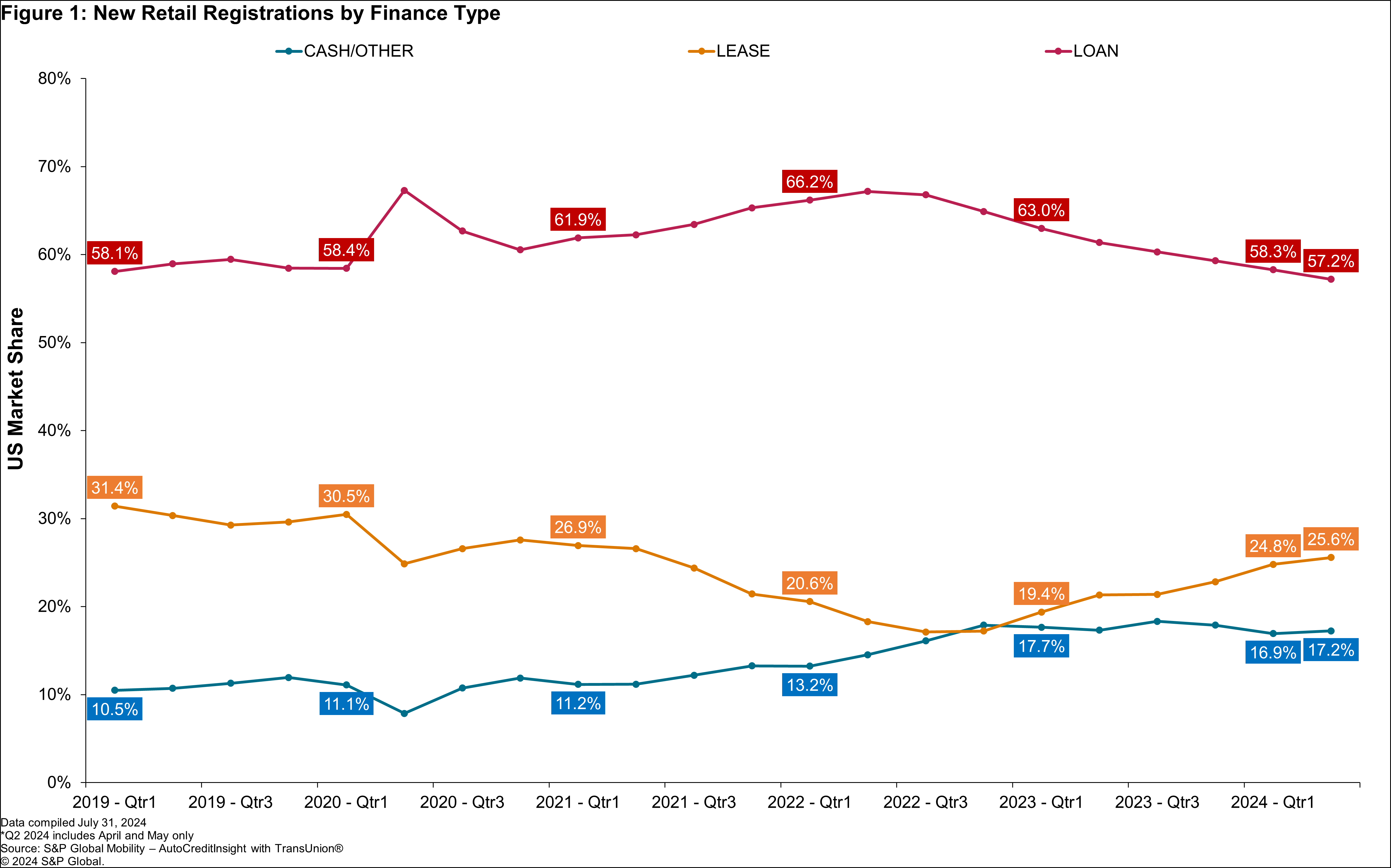

One major tool used to lower prices, particularly for luxury

vehicles, is leasing. We have seen a growing percentage of leased

new vehicles since the second half of 2022, as shown in Figure 1.

From its low point of 17.1% in Q3 2022, lease mix has climbed more

than 8 percentage points to 25.6% this past April and May. Note

that most of leasing gains have come at the expense of loans, while

cash mix has remained relatively stable since the end of 2022.

But federal legislation, and specifically the Inflation

Reduction Act (IRA) signed into law by President Biden in August of

2022, has also contributed to this shift. Specifically, the IRA

allows most EV leases to qualify for a $7,500 tax credit, in

contrast to loans, which have numerous qualifications. These

additional funds provided by the IRA have also enabled dealers to

offer attractive EV lease monthly payments, relative to loan

payments.

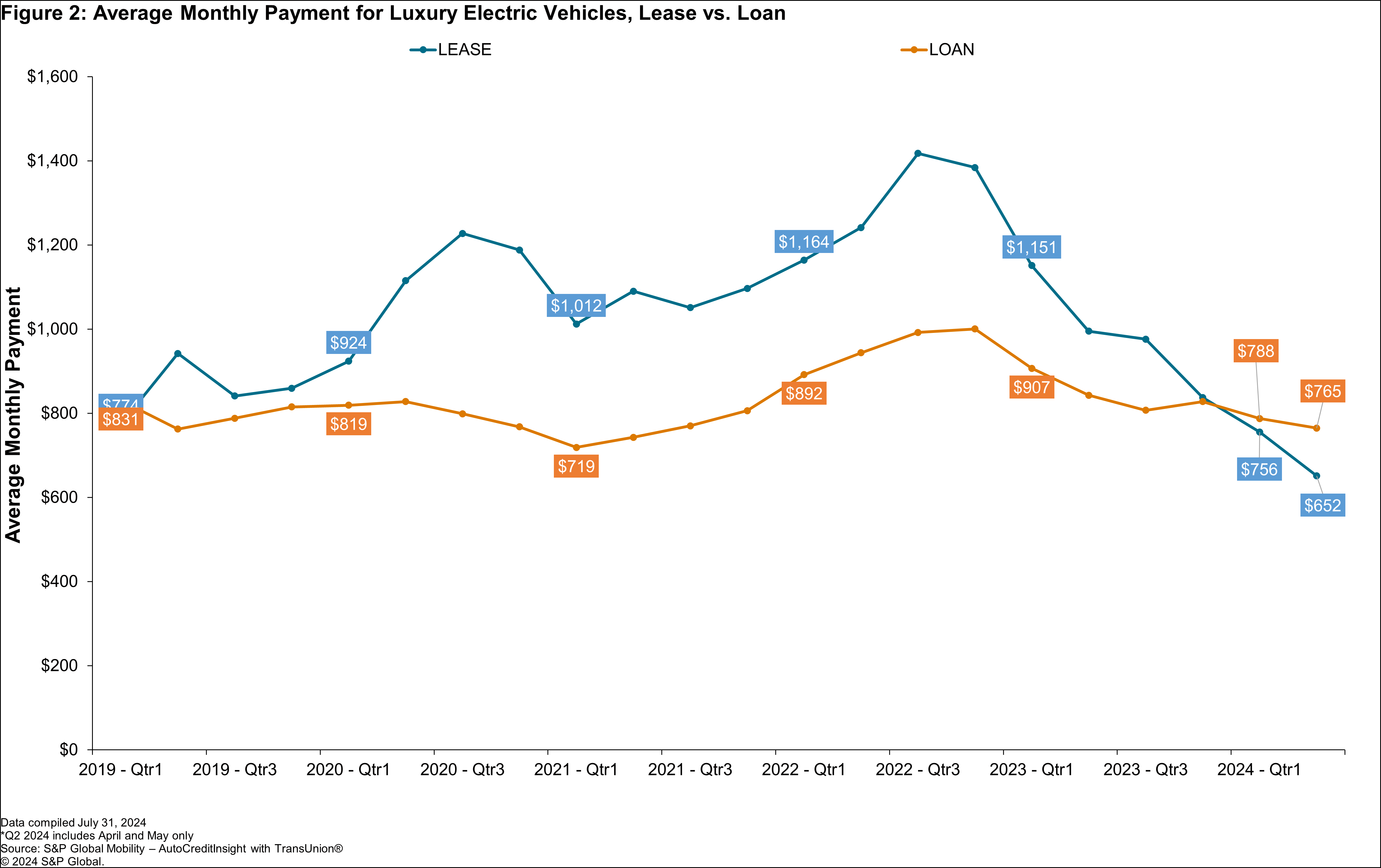

As Figure 2 demonstrates, lease payments for luxury EVs rose

substantially at the start of 2020 when the pandemic arrived and

stayed elevated through much of 2022. But, starting at the end of

2022 soon after the IRA went into effect, lease payments began to

decline both in absolute numbers and relative to loan payments.

And, in the first five months of this year, luxury EV lease

payments have fallen below loan payments (a more normal relative

position for them based on history).

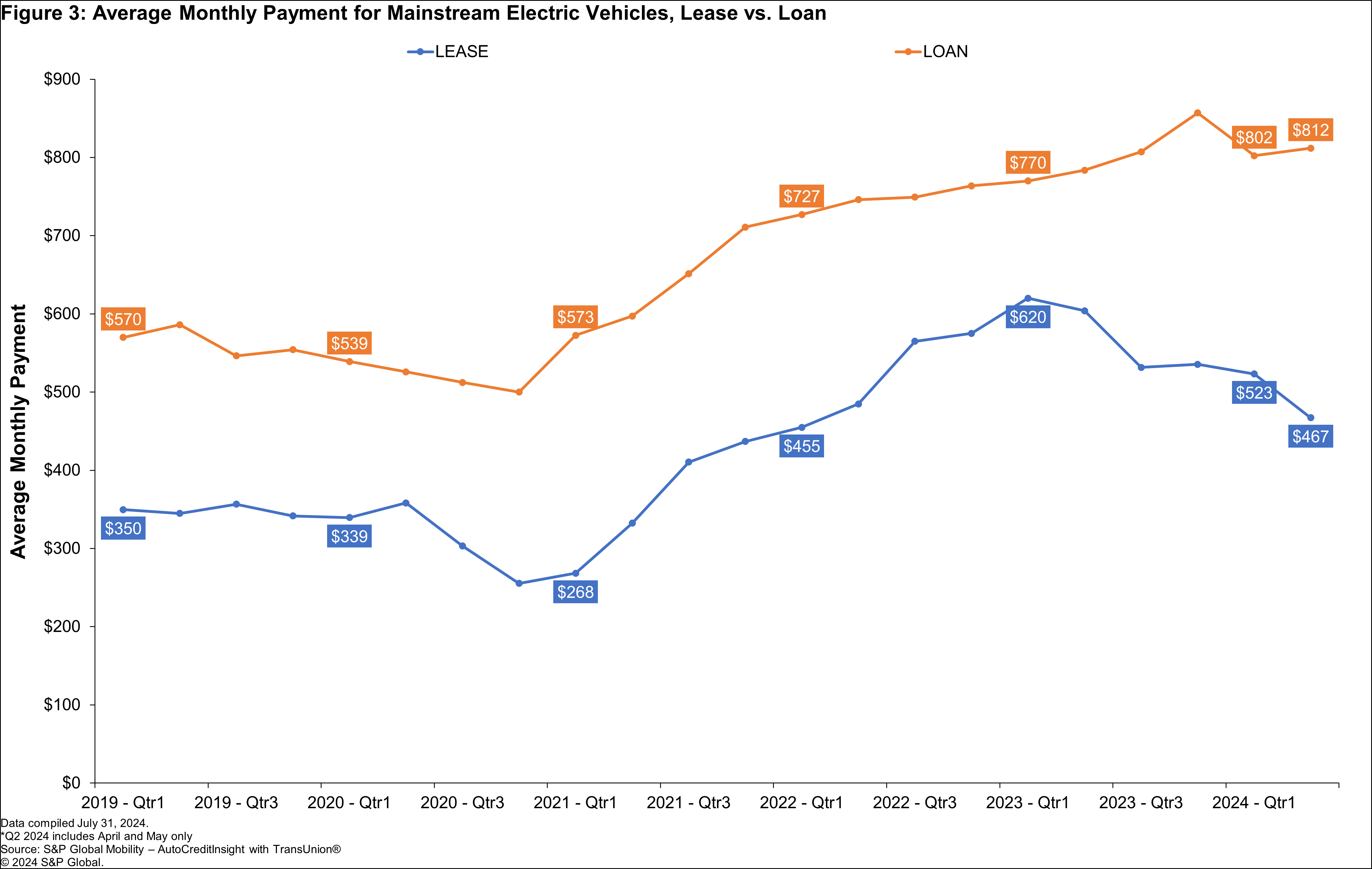

The same trends have occurred in the mainstream EV market, as

illustrated by Figure 3. In the mainstream space, EV lease payments

have been below loan payments throughout the displayed time period,

but the gap began to widen shortly after the IRA adoption date, and

since Q3 2023 the difference between the two metrics has increased

dramatically.

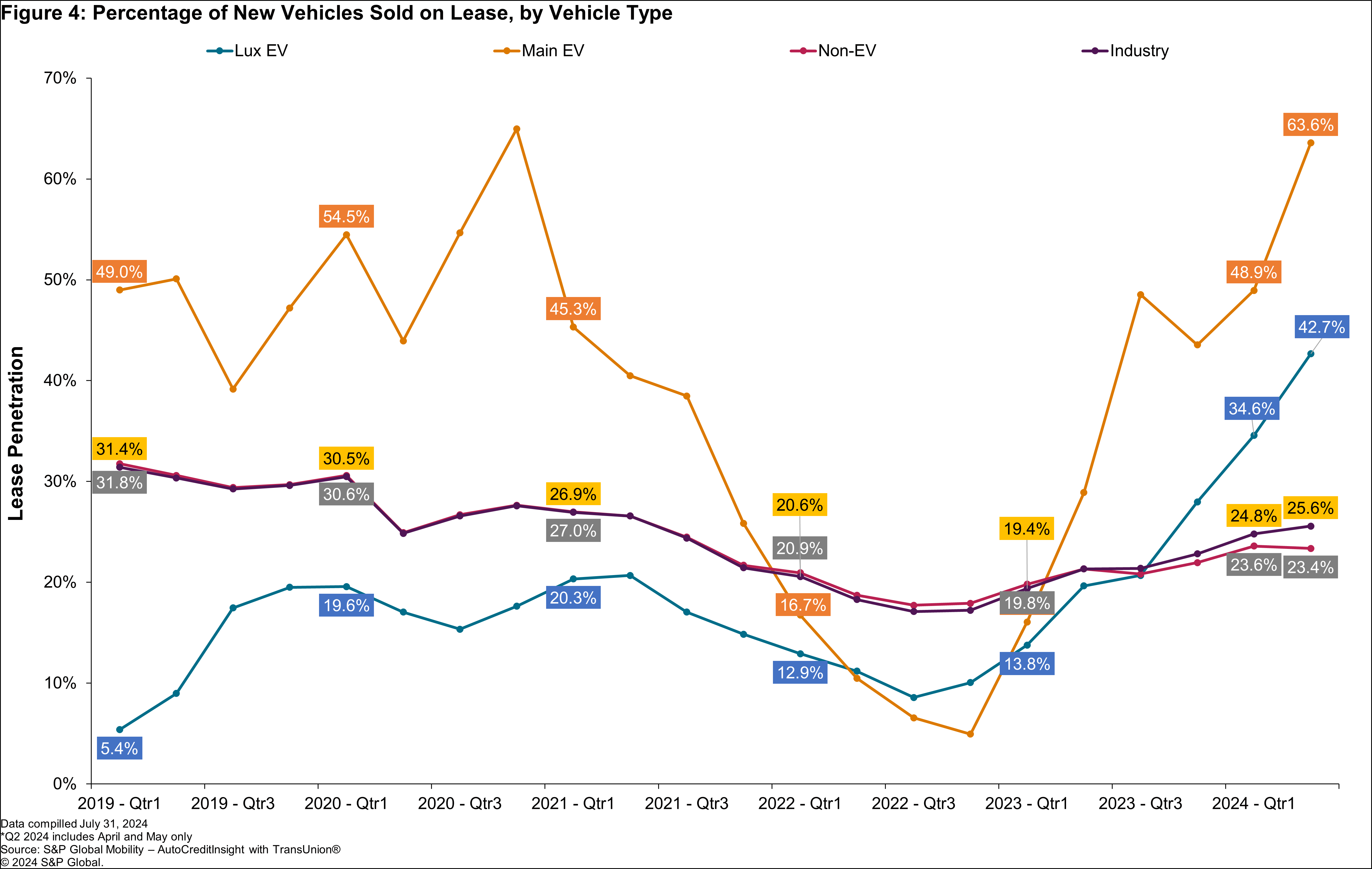

This increased value proposition of leasing EVs, relative to

purchasing them, understandably has driven lease levels to

exceptionally high levels. While industry-wide lease mix has only

risen slightly in the last several months, the EV lease mix among

mainstream products has climbed from 4.9% in Q4 2022 to 63.6% this

past April and May; similarly, lease penetration in the luxury EV

sector has jumped from 8.6% in Q3 2022 to 42.7% in April and

May.

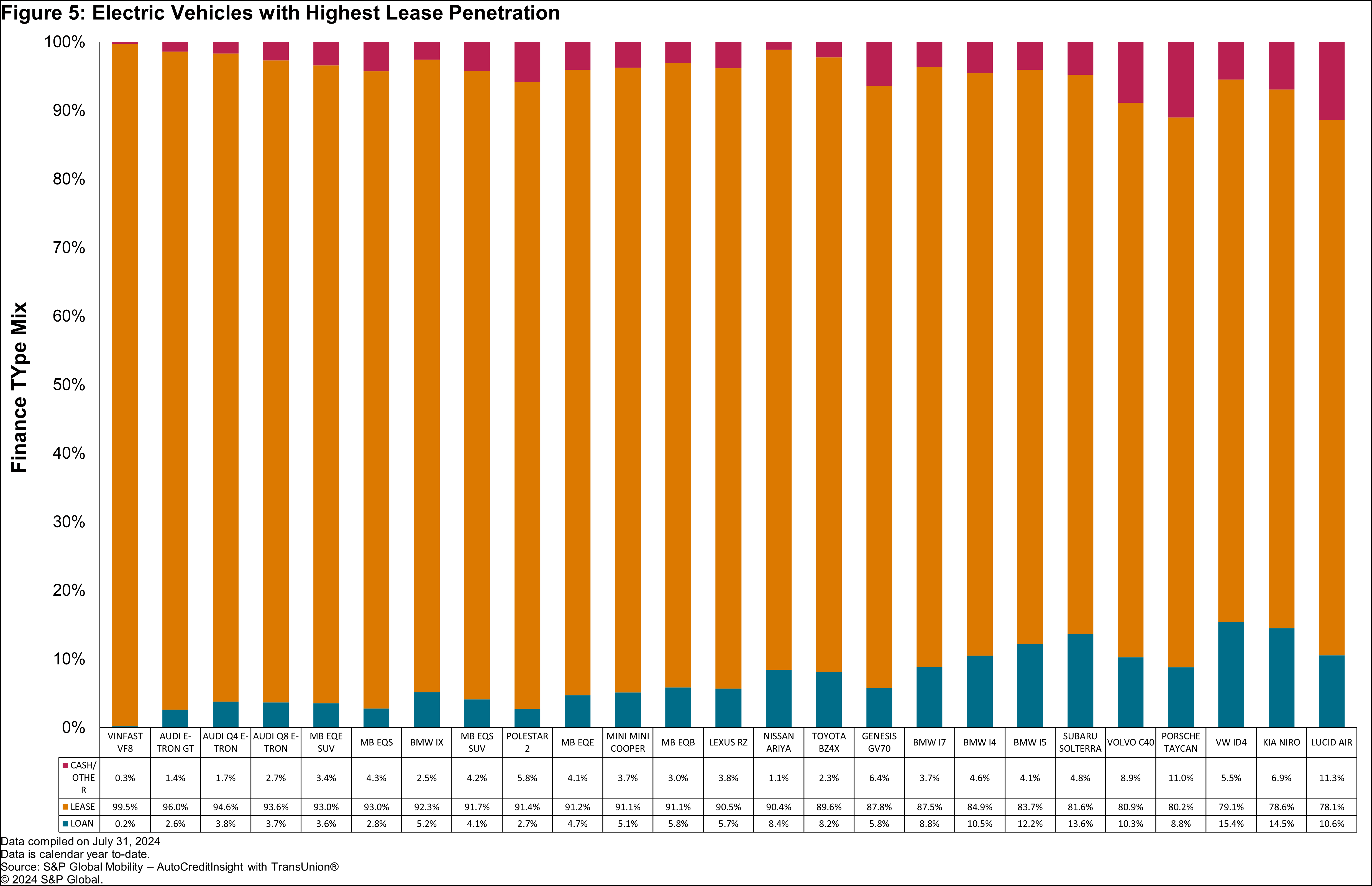

At the model level, these financing dynamics have brought some

extraordinary results. In the first five months of this year, 22

models, including 17 luxury models, had a lease penetration greater

than 80%, and 14 of these models enjoyed a lease mix above 90%.

While the luxury space traditionally has a higher lease mix than

the mainstream market, such a high number of models with

exceptionally high leasing business is rare.

These data point to at least three conclusions. An obvious one

is that if a brand wants to compete in the EV space, it needs to be

an aggressive player in the leasing business. Succeeding in this

endeavor requires an active, established, and competitive captive

finance source.

A second takeaway is that governmental regulations, whether at

the state or national level, can still be used to shift the market

in a direction favored by those in power.

And lastly, these data suggest that the EV market continues to

be in its early stages and therefore subject to rapid fluctuations

depending on regulations, incentives, new models, discontinued

models, other fuel type availability, and the final value

proposition for the consumer.

In partnership with TransUnion, S&P Global Mobility's

AutoCreditInsight™ is the most comprehensive, accurate and timely

vehicle registration and loyalty data with automotive loan

origination activity.